REALTY INCOME (O)·Q4 2025 Earnings Summary

Realty Income Q4 2025: Revenue Beats, AFFO Steady at $1.08, Guides to $8B Investment Year

February 24, 2026 · by Fintool AI Agent

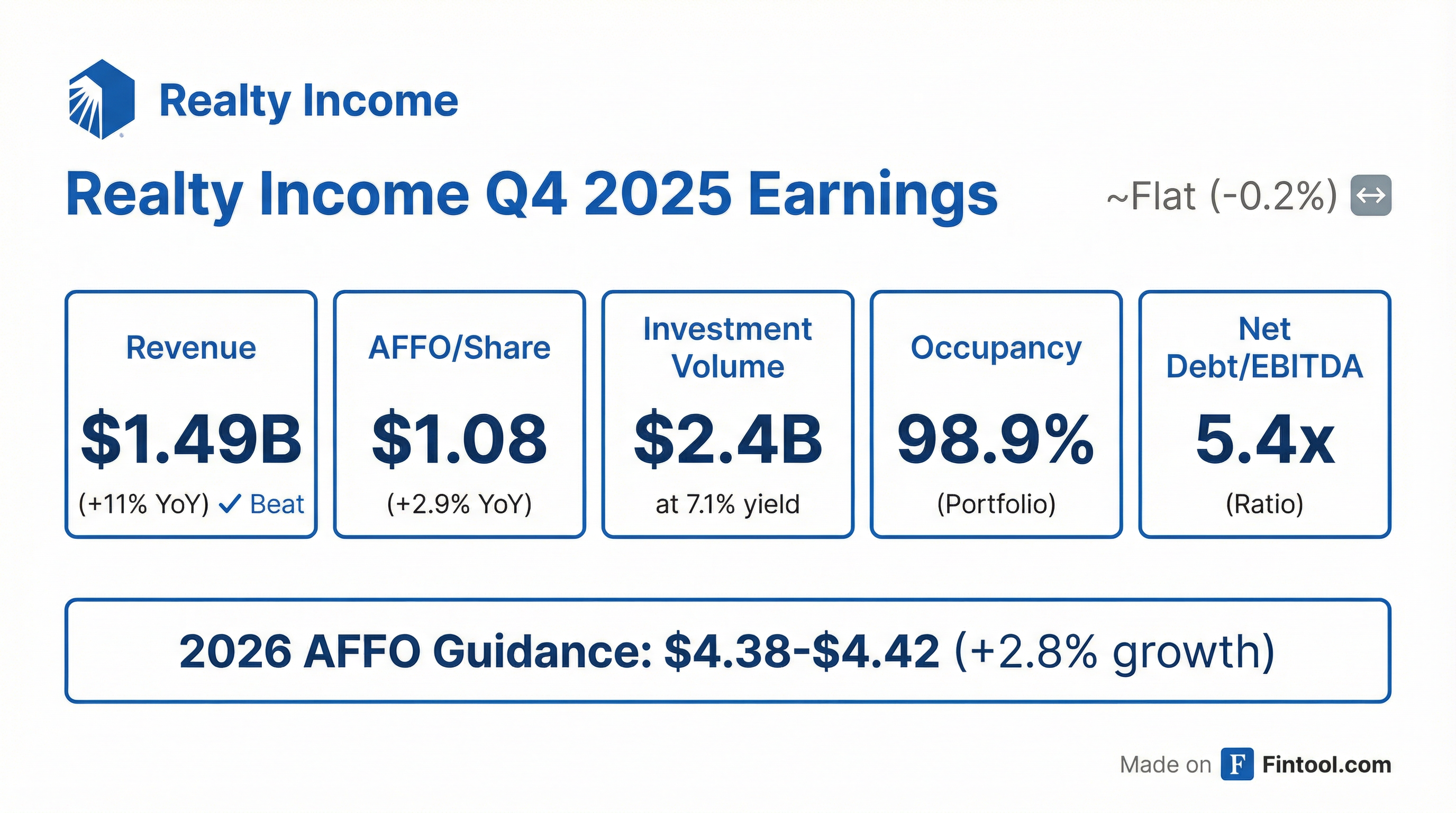

Realty Income Corporation (NYSE: O) reported Q4 2025 results that beat revenue expectations while delivering steady AFFO growth. The triple-net lease REIT posted total revenue of $1.49 billion (+11% YoY) and AFFO per share of $1.08 (+2.9% YoY), reinforcing its position as "The Monthly Dividend Company" with its 113th consecutive quarterly dividend increase.

The stock traded flat on the news, down 0.2% to $66.52, as results largely matched expectations heading into the print.

Did Realty Income Beat Earnings?

Revenue beat, AFFO in-line with expectations. Realty Income delivered Q4 2025 results that exceeded consensus on the top line:

*Values retrieved from S&P Global

For REITs, AFFO (Adjusted Funds From Operations) is the key metric—not GAAP EPS. Realty Income's AFFO of $1.08 per share represents 2.9% growth versus Q4 2024's $1.05.

Full-year 2025 delivered solid execution:

- FY 2025 AFFO per share: $4.28 (+2.1% YoY)

- FY 2025 Total Revenue: $5.75 billion (+9.1% YoY)

- Total investment volume: $6.3 billion at 7.3% weighted average yield

What Did Management Guide for 2026?

CEO Sumit Roy struck an optimistic tone, guiding to accelerated investment activity in 2026:

Key quote from Sumit Roy:

"2025 represented another year of consistent returns and deliberate execution of strategic initiatives that will amplify our competitive strengths. The momentum in our business is palpable. Our fourth quarter investment volume of $2.4 billion represents a meaningful acceleration in activity, and our active pipeline for 2026 is reflected in our initial investment volume guidance of approximately $8.0 billion."

Roy also highlighted a ~9% total operational return for 2026 (AFFO growth + dividend yield), consistent with the company's long-term value proposition.

What Changed From Last Quarter?

Several strategic developments emerged this quarter:

1. GIC Partnership & Private Capital Expansion

Realty Income announced a strategic relationship with GIC (Singapore's sovereign wealth fund) in January 2026, including:

- Build-to-suit development joint venture with $1.5B+ in combined commitments

- Expansion of the company's private capital platform alongside its U.S. Core Plus Fund

2. Mexico Expansion

First investment in Mexico with a $200 million takeout commitment for a USD-denominated, long-term leased industrial portfolio—marking geographic expansion beyond the U.S. and Europe.

3. U.S. Core Plus Fund Launch

Successfully launched inaugural perpetual life U.S. Open-End Core Plus Fund, raising $1.5 billion in total commitments through year-end. The company is capping its cornerstone equity capital raise at $1.7 billion by March 31, 2026.

4. Convertible Notes Issuance

In January 2026, issued $862.5 million of 3.500% convertible senior notes due 2029, using approximately $101.9 million to repurchase ~1.8 million shares concurrently.

How Is the Portfolio Performing?

Realty Income's portfolio remains healthy with steady operational metrics:

Same-store rental revenue growth came in at 1.1% for Q4 and 1.3% for the full year, driven by contractual rent escalators.

Leasing activity was strong:

- Rent recapture rate: 104.9% in Q4 (103.9% full year)

- Re-leased 341 properties in Q4, with 94% to same tenants

How Did Capital Deployment Look?

Q4 2025 saw a significant acceleration in investment activity:

Geographic mix shifted toward Europe:

- U.S. volume: $1.36B (59% of total)

- Europe volume: $951M (41% of total)

Property type allocation:

- Retail: 55% of Q4 acquisitions

- Industrial: 44% of Q4 acquisitions

Notable Q4 investment: $800 million perpetual preferred equity investment in CityCenter's real estate assets (owned by Blackstone Real Estate).

What Is the Balance Sheet Position?

Realty Income maintains conservative leverage with significant liquidity:

Liquidity position: $4.1 billion

- Cash: $419M

- Credit facility availability: $3.5B

- Unsettled ATM forwards: $709M

Credit ratings remain investment grade:

- Moody's: A3 (Stable)

- S&P: A- (Stable)

How Did the Stock React?

The stock was essentially flat on the earnings release, with shares trading at $66.52, down 0.2% from the prior close. This muted reaction suggests the results were largely in line with investor expectations.

Valuation context:

- Current dividend yield: ~4.9% (annualized $3.24/share)

- Dividend payout ratio: 75.2% of AFFO

- 52-week range: $50.71 - $66.92

The stock has rallied significantly from its 2024 lows as interest rate expectations have moderated, with shares up ~10% from the 50-day moving average of $60.05.

What Are the Key Risks?

Management flagged several considerations:

-

Interest rate sensitivity — While 93% of debt is fixed-rate, rising rates impact both cost of capital and cap rate spreads

-

Tenant credit risk — Dollar General and Walgreens represent 3.2% and 3.1% of ABR respectively, with Walgreens facing well-publicized challenges

-

Guidance occupancy decline — Expected occupancy of ~98.5% in 2026 implies 40 bps of deterioration from current 98.9%

-

Currency exposure — 37.8% of debt is non-USD denominated, creating FX translation risk

Forward Catalysts to Watch

-

Q1 2026 investment activity — Management's $8B guidance implies ~$2B/quarter run rate; early pipeline visibility will be key

-

GIC JV ramp — Deployment of the $1.5B+ development partnership

-

Core Plus Fund closing — Targeting $1.7B cap by March 31, 2026

-

Mexico portfolio closeout — Execution on first Latin American entry

-

Interest rate trajectory — Fed policy remains the key external variable for REIT valuations

Key Takeaways

✅ Revenue beat — $1.49B topped consensus by ~3%

✅ AFFO steady — $1.08/share represents 2.9% YoY growth, matching REIT investor expectations

✅ Accelerating deployment — Q4's $2.4B investment run rate supports $8B 2026 guidance

✅ Private capital expansion — GIC partnership and Core Plus Fund diversify capital sources

⚠️ Occupancy guidance softer — 98.5% target implies slight deterioration

⚠️ Walgreens exposure — 3.1% of ABR with tenant under pressure

The print reinforces Realty Income's positioning as a defensive, income-oriented holding with steady mid-single-digit total returns (AFFO growth + 5% dividend yield). The GIC partnership and Core Plus Fund represent meaningful platform expansion that could enhance long-term earnings power.

Related: Realty Income Company Profile | Q3 2025 Earnings | Latest Transcript